Hotel Trends Overview October

Discussion Points to Take Forward

- Many sources cite the recession-like trends in the economy and hotel sector. It is essential to continue monitoring economic growth, tariff impacts, and unemployment rates, as there are key differences between the figures we are seeing today in the sector and those of previous economic recessions.

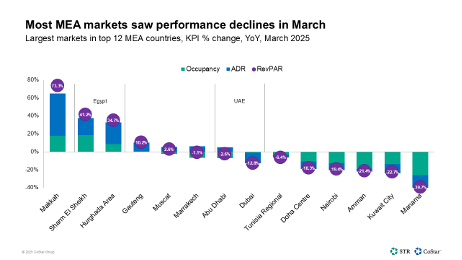

- The US and Parts of Europe are in a hospitality slowdown however globally; the industry is not in a synchronized recession like in 2008. It is a fragmented slowdown shaped by region, segment, and cost, where Asia is stabilizing after a delayed post-COVID boom, and the Middle East/Africa remain growth engines.

- August RevPAR contracted again as weaker ADR growth of 0.4% was offset by a 1.0% drop in occupancy. With the lack of positive momentum on the horizon, the past five months of falling occupancy likely suggest ADR declines later in the year. Keep this in mind while structuring your strategies for the latter half of 2025 into 2026.

- Competition from alternative lodging options continues to hamper hotel demand. Short-term rental RevPAR increased 6% year-over-year in July as ADR rose to 140% of 2019 levels and occupancy remained steady at 101% of 2019.

- Inbound international travel volumes fell again in July. As sentiment shifted, inbound international visitation fell 3.1% y/y in July and is forecasted to continue in this direction through the end of the year. Markets heavily impacted by international travel need to continue to focus on building domestic base volumes.

U.S. Hotels State of the Union September 2025 Edition

Economy

- GDP growth remains below the long-term avg, and inflation remains sticky.

CBRE raised its 2025 GDP forecast to 1.6% from 1.3%. Due to the higher expected base in 2025, CBRE lowered its 2026 GDP growth estimate to 1.8% from 2.0%. Soft top-line growth and elevated inflation will put sustained pressure on hotel profits and margins. - Unemployment remained at 4.2% in line with July 2024.

Real disposable income growth slowed in July to 2.0% while the personal savings rate grew to a healthy 4.4%. Wage gains continue to outpace inflation, suggesting that consumers have money to travel. Unfortunately, RevPAR has continued to decline owing to cannibalization and the loss of inbound international travel. - CMBS volumes decreased, and average loan size fell as interest rates ticked up.

CMBS rates increased slightly up 10bps in July to 7.3% and credit spreads narrowed by 20 basis points y/y. Average loan size fell as well from $102.4 million to $78.8 million as fewer loans were issued with loan count falling to 13 from 24 a year ago.

Current Trends

- After falling 1.1% in July, August MTD RevPAR has fallen 0.6% year-over-year.

August RevPAR MTD contracted again as weaker ADR growth of 0.4% was offset by a 1.0% drop in occupancy. With the lack of positive momentum on the horizon, it is likely that the past five months of falling occupancy suggests ADR declines later in the year. The luxury chain scale outperformed RevPAR gains of 2.3% MTD in August. - STR demand share of 16.0% in July is nearing its pandemic era peak.

STR demand increased again in July, up by 3.6% y/y outpacing the 0.3% decline in hotel demand. Competition from alternative lodging options continues to hamper hotel demand. Short term rental RevPAR increased 6% in July y/y as ADR rose to 140% of 2019 and occupancy remained steady at 101% of 2019. - Operating profits declined 2.7% as costs outpaced total revenue growth in June.

While top line growth outpaced RevPAR growth in June, rising 1.2%, cost increases pressured margins which contracted 0.1 p.p on a TTM basis resulting in declining profits. As weaker revenue growth and higher inflation persist through 2026, we expect margins to continue to be under pressure.

Food for Thought

- Business sentiment remains stable, and earnings growth has been solid.

Despite softer GDP growth and persistent inflation, business sentiment has remained steady at 99 in July while earnings growth is forecasted to increase 13.7% in Q4 2025. On the other hand, consumer sentiment has fallen from 102 in July 2024 to 97 in July 2025, and hotel demand is increasingly consumer reliant. - Inbound international travel volumes fell again in July.

As sentiment shifted, inbound international visitation fell 3.1% y/y in July. Conversely, outbound international travel volumes increased by 6.6%. The imbalance between inbound and outbound travel volumes is likely to persist through 2026, a meaningful headwind to hotel demand. - TSA throughput increased in August by 1.5%.

Throughput growth may accelerate in the back half of the year as comparisons get easier, hopefully leading to more robust RevPAR trends. Google searches for corporate and redemption travel increased again in August, up 6.4% and 3.3% y/y, respectively, suggesting stronger travel trends in the fall. - The S. and parts of Europe are in a hospitality slowdown / mini-recession phase.

- Asia is in post-boom stabilization.

- Middle East & Africa remain growth engines.

- Globally, the industry is not in a synchronized recession like 2008 — it’s a fragmented slowdown shaped by region, segment, and cost structure.

Global Context — Summary (as of late 2025)

North America (U.S. & Canada):

- Experiencing what analysts call a “sectoral recession,” RevPAR growth nearly flat, business and group travel soft, cost inflation persistent, and leisure remains decent but no longer compensates for weak corporate demand.

- Closest resemblance—mild version of 2001, not as catastrophic as 2008.

Europe:

- Patchy performance. Southern Europe (Spain, Portugal, Greece) still buoyed by leisure and international demand, but Northern/Central Europe (Germany, UK, France) are slipping into mild recession due to slower business travel and high energy costs.

- Inflation has eroded margins even where occupancy is stable, but overall it is a stagnation rather than collapse (flat RevPAR with profit squeeze).

Asia-Pacific:

- China & Japan: uneven; domestic tourism strong, but outbound and inbound still below 2019 levels; Southeast Asia: resilient leisure markets (Thailand, Vietnam, Indonesia) offsetting weak corporate travel.

- Not in recession, but still in a slow normalization cycle post-COVID rebound.

Middle East / Gulf / Africa:

- Still growing, thanks to massive event-driven demand (Saudi Vision 2030, Dubai tourism push, African urban growth).

- Far from recession—in fact, these regions are the global outliers with double-digit RevPAR gains.

Signs point to an “industry-specific” recession for hospitality, but not (yet) a full economy-wide collapse like in 2008.

- The drivers today differ meaningfully from previous recessions, which alters both risk and recovery dynamics.

- In 2001 the trigger was a combination of economic slowdown + the shock of the September 11th attacks. com+1

- In 2008 the trigger was financial crisis + credit collapse + macro recession—leading to sharp consumer/business demand. VTechWorks+1

- Today: we’re seeing inflation, high costs, shifting consumer travel patterns, weakening business travel, and international visitation slower — but we haven’t yet seen a deep credit collapse or full GDP contraction in the U.S. lodging segment. CoStar+1

- Because the triggers differ, this means playbook from 2001/2008 may not fully align—the decline might be slower, more structural (consumer behavior shift), and recovery may be different.

Despite the pressure, some resilience exists — so the situation is nuanced, not uniformly dire.

- Even in the current environment: unemployment is low, consumers are still traveling (especially for leisure), and there is a degree of pricing power in some segments. CoStar

- The hospitality downturn is uneven: luxury brands may fare better; some markets are stronger than others. In 2008/09 the pain was more broad-based. Pinnacle Advisory Group+1

- Thus: one could argue we are in a “sectoral meltdown risk” rather than universal collapse—meaning it’s possible to outperform if you’re agile, cost-efficient, correctly positioned, and adaptive.

Bottom line: For the hospitality business, I’d say: yes, we’re in a recession‐like state in many respects—weak demand growth, pricing pressure, cost headwinds—but not on the scale or abruptness of the 2008 recession, and different in nature from the 2001 event. That means we should treat this as a serious risk phase: act proactively but not assume a simple repeat of past patterns.

- The drivers today differ meaningfully from previous recessions, which alters both risk and recovery dynamics.

- Hospitality industry growth on a global scale is still positive, driven by stability in the Asian region, and growth in Africa and the Middle East, offsetting losses in the US and Europe.

- Even in the current environment, unemployment is low, consumers are still traveling (especially for leisure), and there is a degree of pricing power in some segments. Focus on these segments, particularly within the domestic market, when looking ahead.