State of the Industry Report

Alexandre Sinclair, Director of Revenue Strategy and Commercial Analytics

Hotel Trends Overview May 2026

As we move into the middle of 2026, economic uncertainty, evolving guest expectations, and shifting consumer spending patterns are at the forefront of hospitality. The section below highlights the latest performance benchmarks, emerging market dynamics, and key risks facing hoteliers. Whether you operate in major metropolitan markets or leisure destinations, understanding these trends is critical for maximizing revenue opportunities and preparing for what’s ahead.

Core Economic Performance & Benchmarks

- Economic Output: Q1 2026 GDP expanded at a 2.0% annual rate, a notable acceleration from the sluggish 0.5% growth recorded in the final quarter of 2025.

- Inflation Dynamics: The Consumer Price Index (CPI) hit 3.3% in March, signaling that price pressures are more “sticky” than the 2.6% levels seen during parts of 2025.

- Employment Landscape: The jobless rate has ticked up to 4.5%, compared to the tighter 3.8%–4.0% range maintained throughout much of 2025.

- Capital Expenditure: A massive 8.7% jump in AI-driven business spending is currently the primary engine of growth, offsetting weaker housing data.

- Monetary Policy: Interest rates remain at multi-decade highs, as the Federal Reserve has been unable to mirror the rate-cut optimism that permeated the markets in late 2025.

Consumer Behavior Forecast

- Growth Deceleration: Real consumer spending is on track for 2.1% growth this year, a clear step down from the 2.7% expansion seen in 2025.

- The “Spending Divide”: 2026 is defined by a bifurcated market; wealth effects from the stock market are fueling luxury spending, while essential costs are draining the savings of lower-income groups.

- Energy Impact: Rising fuel and utility costs in early 2026 have replaced supply chain issues as the primary deterrent to discretionary retail shopping.

- Credit Constraints: Household debt and delinquency rates for credit cards have risen significantly compared to 2025 averages, leading to stricter lending standards.

- Service Preference: While goods spending remains flat, demand for travel and experiences continues to outperform, though at a slower pace than the 2025 “revenge travel” peak.

Continued Economic Trends Impacting Domestic and Global Tourism

Potential Headwinds

- Regional Instability: Energy price shocks originating from Middle Eastern tensions remain the largest threat to the 2026 inflation outlook.

- Trade Policy: New discussions around USMCA revisions and potential tariffs have introduced a layer of corporate uncertainty that was less prevalent in 2025.

- Housing Stagnation: The residential sector continues to struggle, marking over a year of consecutive contraction due to high mortgage rates.

Key Economic Impacts (Q1 2026):

- Inflation: The Personal Consumption Expenditures (PCE) price index rose to 3.5% annually in March, up from 2.8% in February.

- Energy Prices: Gasoline prices have surged, with average prices rising more than $1 per gallon this year.

- Market Volatility: Oil prices have experienced high volatility, with disruptions in the Middle East threatening global supply.

- Oil Prices: Benchmark global oil futures surged, with crude oil reaching over $100 a barrel.

- Consumer Confidence: Sentiment reached record lows, even falling below pandemic-era levels, driven by higher costs at the pump.

- Job Market: The labor market showed signs of slowing, with 133,000 jobs lost in February but recovering with 178,000 jobs added in March.

- Cost to Consumers: The war has increased expenses for households by about $150 per month on average for fuel and fertilizer.

U.S. Market Outlook 2026

As of May 2026, the American lodging sector is exhibiting steady expansion, marked by a balance between consumer demand and a cautious approach to new developments.

Although several metropolitan hubs are still working to match the high-water marks set in 2019, key regions—particularly San Francisco and major vacation spots—are demonstrating robust momentum.

CBRE’s latest quarterly analysis indicates a transition toward reliable, incremental progress:

- Occupancy Levels: Saw a 0.8% annual uptick, as a 2.0% rise in guest interest effectively absorbed a slim 0.6% expansion in available rooms.

- RevPAR Growth: Climbed 3.8%, a figure bolstered primarily by the upward movement of nightly pricing.

- Average Daily Rate: Registered a 2.2% increase year-over-year.

- Inventory Constraints: New construction is expected to remain tight, holding at under 1% growth through 2029 due to elevated borrowing rates and material expenses.

Success in the current landscape depends heavily on specific geography and property class:

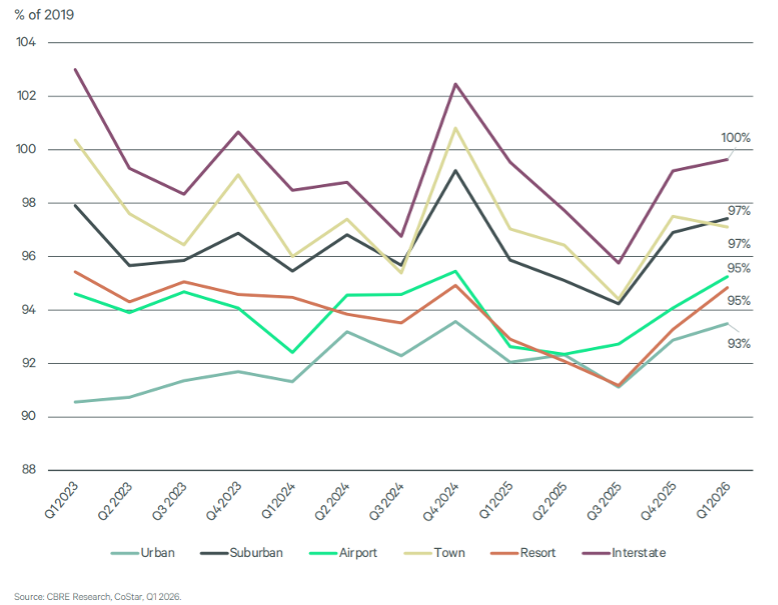

- City Centers: Metropolitan hotels have regained roughly 93.5% of their historical occupancy capacity.

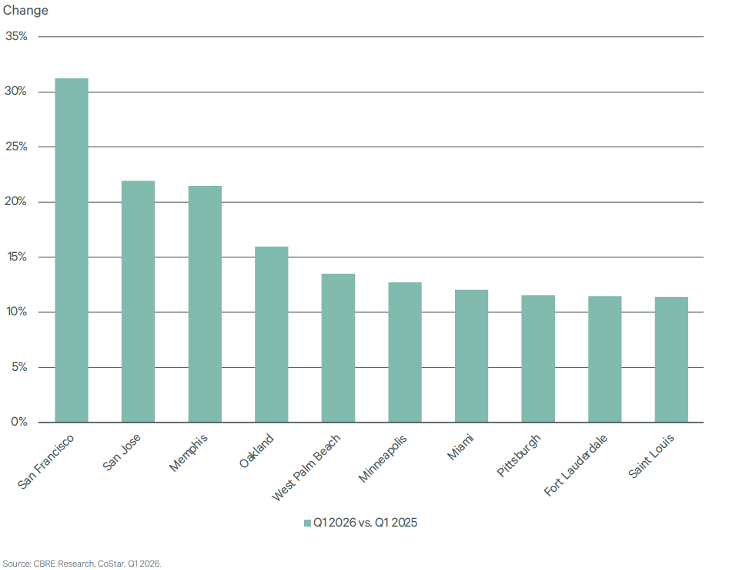

- Standout Cities: San Francisco saw a massive 31% spike in RevPAR this past quarter, largely attributed to a resurgence in tech-sector business trips.

- Reliable Segments: Upper-midscale properties remain the most consistent performers for stakeholders.

- Growth Catalysts: Massive international events, including the 2026 World Cup, are projected to keep RevPAR gains between 1.5% and 3.5% for the foreseeable future.

Top 10 markets for year-over-year RevPAR growth

- Transaction Totals: Forecasts suggest a 16% jump in capital allocation for commercial property, potentially hitting $562 billion.

- Buyer Confidence: Roughly three-quarters of major investors intend to expand their portfolios during this calendar year.

- Credit Access: Traditional lenders are predicted to step back into the arena, providing much-needed capital for hotel purchases.

- Beyond U.S.

- European Markets: Expect a modest 1% to 3% RevPAR lift, fueled by a 10% jump in cross-border corporate meetings.

- Asia Pacific: Emerging hubs like Mumbai are hitting record-high occupancy levels thanks to a boom in domestic tourism and large-scale conventions.

Occupancy indexed to 2019 by location type

Gains in Air Travel at risk due to rising costs

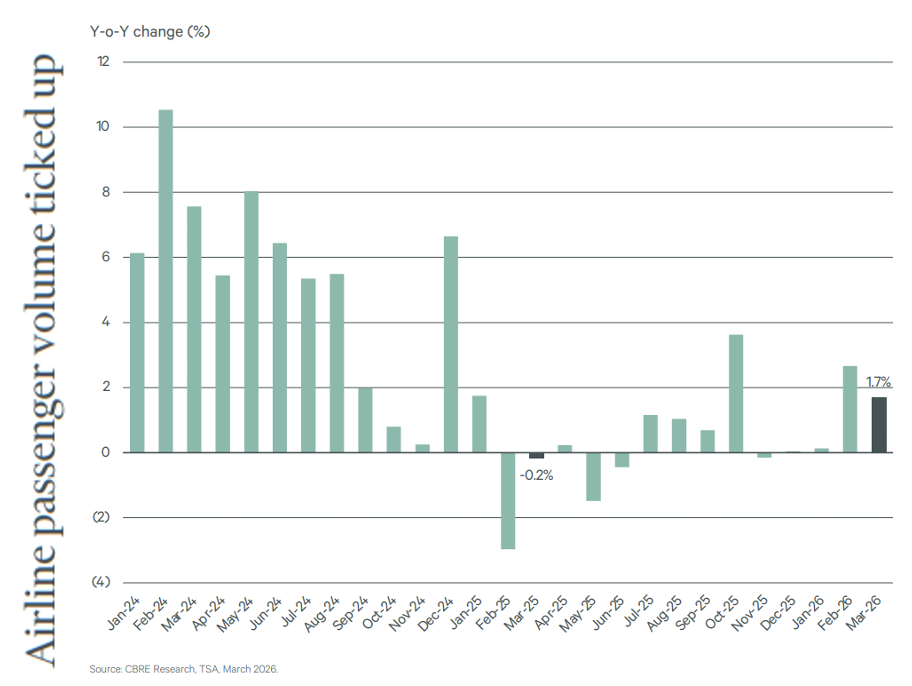

- Passenger volume in Q1 rose by 1% year over year and was 8% above Q1 2019 level. However, spiking jet fuel prices caused by the Middle East conflict pose a risk for air travel growth.

- The conflict is projected to significantly weaken inbound tourism for the next 12 months, primarily due to price increases. However, some experts believe that the conflict will strengthen domestic tourism.

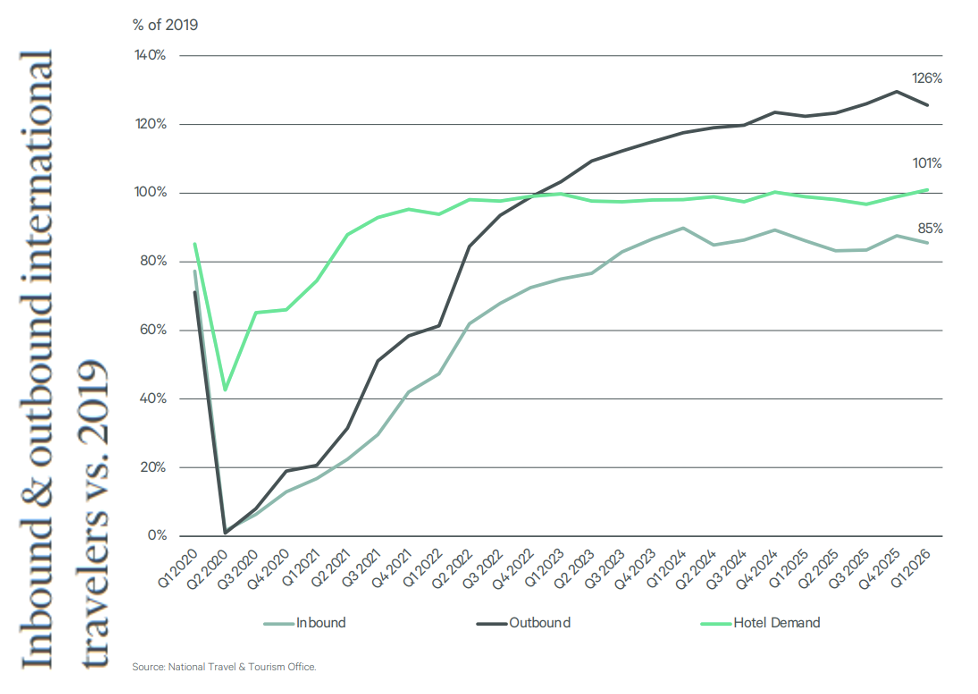

- Inbound international visitation in Q1 remained at 85% 0f Q4 2019 levels, while outbound travel volume reached 126%.

- Costs remain a significant barrier due to consumers spending larger proportions of income on living costs. Consumers are expected to continue seeking better value for money while traveling

- Growth confidence remains stable on medium and long-term horizons but has fallen sharply for short-term. Visitor numbers and hotel occupancy have subdued compared with last quarter but are still expected to increase slightly in 2026.

- Growth Deceleration: Real consumer spending is on track for 2.1% growth this year, a clear step down from the 2.7% expansion seen in 2025.

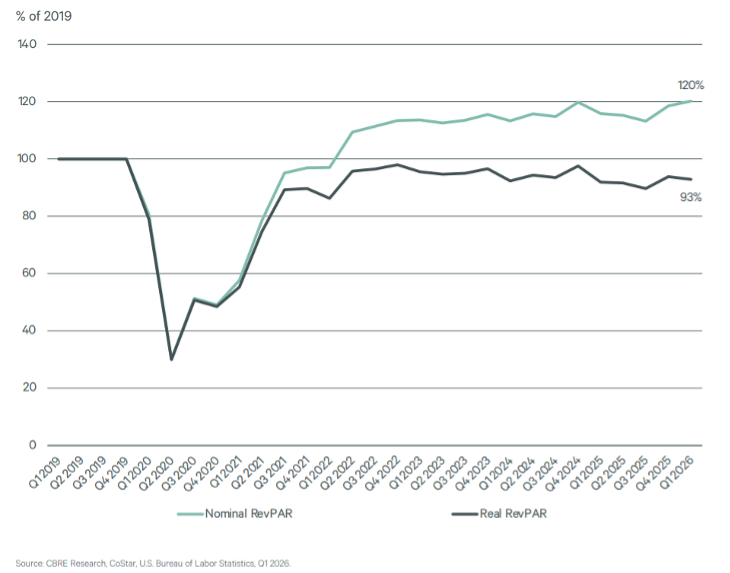

- While Nominal RevPAR growth is still positive in the US since 2019, the Real RevPAR growth is -7% once inflation is factored in

- The conflict in the Middle East is set to significantly weaken inbound tourism for the next 12 months to the US, primarily due to price increases. However, some experts believe that the conflict will strengthen domestic tourism.

- Tariff negotiations continue to play a role in the market outlook, which introduced a layer of corporate uncertainty that was less prevalent in 2025.

Conclusion:

The hotel industry faces both promising growth and definite challenges. Success will depend on a proactive approach to revenue strategy, keen monitoring of global and domestic developments, and the continuous delivery of value to guests. The Revenue Matters Team remains committed to keeping our clients informed and adaptable as the industry evolves.

{kind=link}