State of the Industry Report

Alexandre Sinclair, Director of Revenue Strategy and Commercial Analytics

Discussion Points to Take Forward

Inbound travel to the US lags behind in 2019 and is not expected to return in 2025. Strategies should continue to focus on domestic vs. international POS.

GDP growth and consumer spending are expected to decelerate in 2025, with a growth of 2.1% vs. 2.4% in 2024. This is important to review with hotels to align growth expectations year over year.

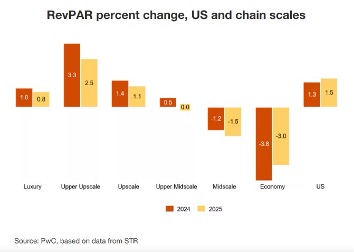

ADR performance gains are expected to average 1.3% in annual growth for 2025, resulting in a yearly ADR-driven increase of 1.5% in RevPAR

Group demand continues to increase year–over–year, driven by conventions and corporate meetings. Crossover numbers have returned to pre-COVID levels. Review with your DOS how hotel crossover numbers for 2025 compared to 2019.

U.S. Hotels State of the Union January 2025 Edition

Current Trends

- November RevPAR increased 0.6%, slightly below the YTD average of 0.8%. While ADR continued to lag inflation, both ADR and occupancy increased in November. As a result of easier prior-year comparisons, lower-priced hotel RevPAR growth outperformed. All location types, except Resorts, posted y/y RevPAR gains in November.

- Short-term rental demand grew 5.1% in November. STRs continued to take share from hotels, with demand rising 5.1% compared with a 0.8% increase in hotel demand. STR demand share reached a post-pandemic high of 14% in November compared with 13% a year ago. Higher interest rates and increasing supply are leading to slowing inventory growth, with supply rising 2.3% in Nov. 2024, down from 10.4% a year ago.

- October’s total hotel revenues were above the 2.1% YTD trend. A pull forward of demand related to the election may have led to a 4.0% increase in total revenues in October 2024, supporting a 3.4% increase in profit dollars. While costs have started to moderate, on a trailing twelve-month basis, margins contracted 0.8 p.p. despite a 1.7% increase in total revenues.

Food for Thought

- Hotel wage growth moderated to 3.1% in October. Hotel wage growth slowed to 3.1% in October 2024 from 5.0% in October 2023 despite an increase in job openings per hotel. Job openings per hotel were 17.2 as of October 2024, above 15.5 during the same period in 2019, and below 18.5 a year ago.

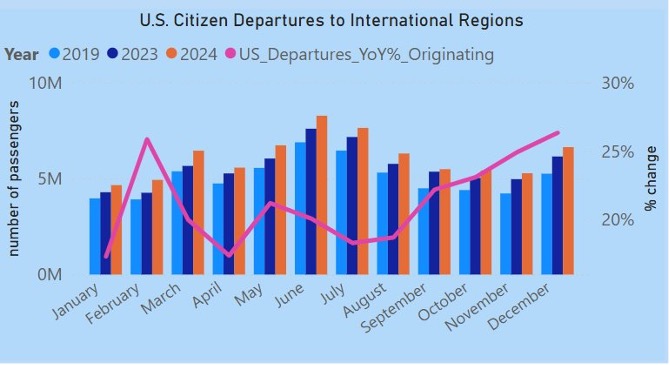

- Inbound international travel has stalled at roughly 90% of 2019 as of November. Outbound international travel increased to 122% of 2019’s level in November, while inbound lagged at 88%. Given the recent mid-single-digit growth trends, it is unlikely that inbound international travel will fully recover in 2025.

- TSA throughput rebounded in December, up 6.5% y/y. December’s 6.5% increase was well above the recent near-zero growth trends, signaling a strong holiday travel season. RevPAR performance of airport hotels had slowed in November, but stronger December throughput could signal stronger trends ahead.

RevPAR Highlights

- Growth in 2025 is expected to be muted due to decelerating consumer spending and GDP growth, projected to increase by an annual average of 2.7% and 2.1% in 2024 and 2025, respectively.

- Despite the continuing growth in business travel, particularly meetings and group business, international travelers to pre-COVID levels, economic challenges are expected to continue to impact leisure travel.

- This outlook may shift as the current political and economic uncertainty landscape becomes more apparent in the coming months after the recent election, including the potential impact of immigration policies, evolving travel patterns and restrictions, and tariffs.

- ADR performance gains are expected to average 1.3% in annual growth for 2025, resulting in a yearly ADR-driven increase of 1.5% in RevPAR. Significant risks to this outlook include the pace of changes in the macroeconomic environment, the pace of rate cuts, the evolution of monetary policy, and the impact of policy implementation after the recent election.

Will international inbound demand rebound?

The data shows the impact of a strong dollar on consumer behavior. By November, international inbound passengers stood at 54.3 million, around 8.8% below 2019 results. Americans, however, went abroad with abandon, and the 66.7 million outbound traveler count is 21% above pre-pandemic results.

Members of the incoming administration have been vocal about their desire to stem and reverse illegal immigration. However, the rhetoric surrounding foreigners can have unintended consequences, and President Trump’s first term shows how it can affect travel flows. Oxford Economics analyzed international visitors to the US between 2017 and 2019 and showed that inbound travel growth slowed. For some areas of origin, such as Mexico or the Middle East, the number of international visitors declined.

Given the expected rhetoric from the White House and a continued strong dollar, international inbound demand is unlikely to rebound to pre-pandemic levels.

Questions and answers for the US hotel industry in 2025

Will room rate growth beat inflation?

The CoStar forecast is clear: We expect the average daily rate to grow by 1.6% in 2025. Oxford Economics proposes that the rate of inflation in 2025, as measured by the Consumer Price Index, will increase by 2.6% as of their December release. In other words, operators’ top line will not rise as fast as costs, which will likely affect the bottom line.

Higher-end hotels will continue to increase rates a little faster than lowering them. The luxury ADR forecast stands at 1.9%, while the economy chain-scale ADR forecast shows 0.2% growth. We do not think prices will rise above CPI levels.

Will small meetings continue to drive full-service hotel results?

Through October, group occupancy for hotels with more than 1,000 rooms has grown by only 1%. For smaller hotels, with a room count between 300 and 500, the group occupancy growth was 2.7%. Many meetings have 100 people or fewer on peak nights and only meet for a night or two.

One common issue revenue managers point out is that bookings for these smaller groups are not “in the quarter, for the quarter” but “in the month, for the month,” so they are very hard to plan and forecast for.

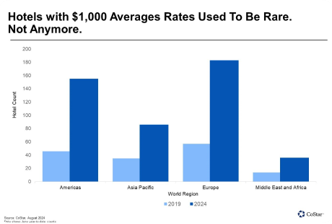

Will the number of hotels with ADR of over $1,000 continue to rise?

These rates are out of reach for the ordinary traveler, but the less than 100 hotels in the U.S. that reported an ADR of over $1,000 in 2024 are catering to a very slim subset of consumers. When we look at our pipeline of new resorts and city hotels opening in the coming year, more high-end hotels will “join the club.”

We fully expect that the number of hotels with an ADR of over $1,000 will increase in 2025.

More Hotels Around the World Report an Average Rate of Over $1,000

- Strong leisure demand from high-end travelers has supported robust hotel pricing increases. This translates to more hotels that can regularly charge well over $1,000 per room per night and are reporting an average daily rate, or ADR, of over $1,000 for the first half of the year.

- In the same period in 2019, around 150 hotels globally reported an ADR of over $1,000. This year, that number has jumped to 460 hotels.

- Operators yielded the more desirable room types, such as suites with multiple bedrooms, due to a report that in 2020, many of their guests felt unable or unwilling to travel and that in the following years, they wanted to make up for lost time. In addition, the strong desire to be with loved ones and family members gave rise to multigenerational trips, requiring more and more extensive accommodations.

- The increase in hotels charging four-digit ADRs is a global phenomenon. Since 2019, the number of hotels in that price range has tripled in the Americas and Europe and more than doubled in the Asia Pacific, Middle East, and Africa regions. This speaks to the proliferation of higher-end brands and the global nature of high-end leisure demand.

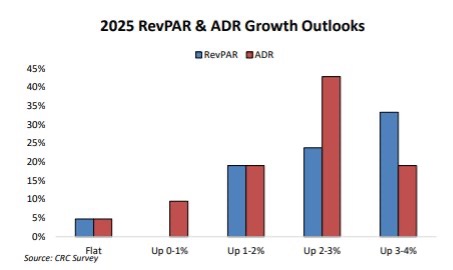

- 2025 outlooks point to ~2.5% RevPAR growth driven by ADR.

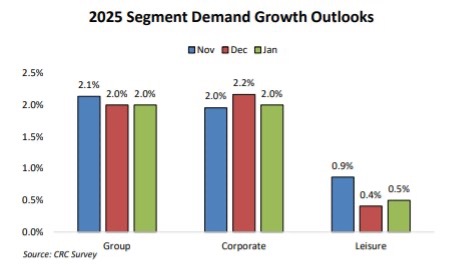

- Our latest survey points to weighted average group/corporate demand up ~2% for ‘25, similar to prior outlooks. Group demand pace sounds up LSD for ’25 at similar crossover levels to pre-COVID (60-70% on the books). Group demand is expected to be driven by conventions and corporate meetings.

- Corporate outlooks do look better for managed corporate relative to SMB.

- Leisure outlooks point to growth of sub 1%. Based on our industry demand estimates, these outlooks suggest ~1.5% total US demand growth for ’25.

- ADR remains the key driver to ’25 RevPAR growth in current budgets. Our latest survey leans more positive on RevPAR growth, now up 2.5%+ (prior up 2.0-2.5%), and weighted average ADR growth is up 2.1%. We are now estimating 2.5% RevPAR growth (prior 2%).

As of November, inbound international travel stalled at roughly 90% of 2019 as of November while outbound international travel increased to 122%. Given the recent mid-single-digit growth trends, it is unlikely that inbound international travel will fully recover in 2025.

Growth in 2025 is expected to be muted due to decelerating consumer spending and GDP growth, projected to increase by an annual average of 2.7% and 2.1% in 2024 and 2025, respectively.

ADR performance gains are expected to average 1.3% in annual growth for 2025, resulting in a yearly ADR-driven increase of 1.5% in RevPAR.

The average group/corporate demand is up ~2% for 2025, similar to prior outlooks. Group demand pace sounds up LSD for 2025 at similar crossover levels to pre-COVID (60-70% on the books). Group demand is expected to be driven by conventions and corporate meetings.

Sources