Alexandre Sinclair, Director of Revenue Strategy and Commercial Analytics

Discussion Points to Take Forward

Inbound travel to the US lags behind in 2019 and is not expected to return in 2025. Strategies should continue to focus on domestic vs. international POS.

GDP growth and consumer spending are expected to decelerate in 2025, with a growth of 2.1% vs. 2.4% in 2024. This is important to review with hotels to align growth expectations year over year.

ADR performance gains are expected to average 1.3% in annual growth for 2025, resulting in a yearly ADR-driven increase of 1.5% in RevPAR

Group demand continues to increase year over year, driven by conventions and corporate meetings. Crossover numbers have returned to pre-COVID levels. Review with your DOS how hotel crossover numbers for 2025 compared to 2019.

U.S. Hotels State of the Union March 2025 Edition

Economy

- CBRE forecasts 4% 2025 GDP growth above the 2.1% long run. Inflation is expected to decrease in 2025, dropping to 2.5% from 2.9% in 2024. The Fed Funds Target Rate is expected to decrease to 80 bps by the end of 2025 to 3.9%. Employment is expected to pick up in 2025, increasing by 0.6%.

- Employment gains in January were the strongest since Q4 2023. Employment rose 1.7% in January, and wages grew 4.1%, around 106 bps higher than inflation. However, the 7.1% and 4.5% increases in airfares and RevPAR could be a travel headwind. Disposable income growth slowed to 1.8% in January.

- CRE delinquency rates surpassed that of hotels for the first time in January. In January, lodging delinquencies were 6.2% lower than the overall CRE delinquency rate, which stood at 6.6%. Special servicing rates rose 130 basis points year-over-year from 6.9% in January 2024 to 8.2% in January 2025.

Current Trends

- January RevPAR increased 4.5%, driven by increases in rate and occupancy. A 4% increase in ADR and a 1.0% increase in occupancy led to another month of strong RevPAR growth. Sporting events, natural disasters, and the inauguration helped to boost rates and occupancy in January, particularly for luxury hotels, which experienced a 12% increase in RevPAR.

- Alternative lodging sources continue to take shares from traditional hotels. The short-term rental demand share reached 13.5% in January 2025 compared with 11.3% at the beginning of 2020. Similarly to hotels, short-term rentals experienced strong rate growth and occupancy expansion in January, with RevPAR increasing 8.1%.

- Profit dollars increased 11.8% in December, far outpacing the full-year trend of -0.2 %. Strong RevPAR growth in December resulted in the highest total operating revenue increase since March 2023, up 6.4%. Despite mid-single-digit revenue growth supporting margin expansion in December, expense growth outpaced total revenue growth in 2024, resulting in a 0.4 pp. contraction in TTM profit margins and declining profits in 2024.

Food for Thought

- CBRE forecasts RevPAR growth of 2.0% in 2025, accelerating to 6% in 2026. In 2025, CBRE expects a 1.6% increase in ADR and a 0.3% increase in occupancy to result in a 2.0% growth in RevPAR. Urban locations are expected to outperform other location types, driven by improved international inbound travel and increased business transient and group travel.

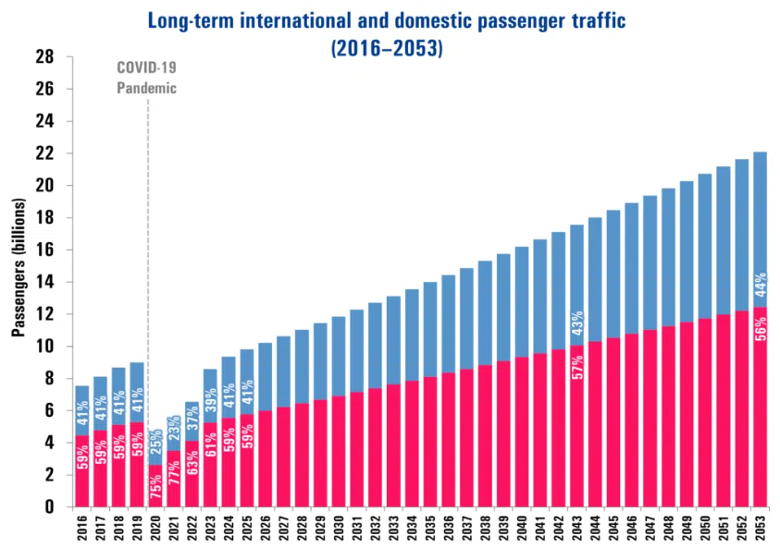

- International travel imbalance unlikely to normalize in 2025. Outbound international travel rose 8.5% y/y, outpacing the 4% y/y growth in inbound visitation, making normalization of the international travel imbalance unlikely in 2025. The growth rate of inbound visitation to East and West Coast markets has slowed materially since last year. Travel from Japan and China is slowly recovering.

- TSA throughput is up slightly 1.0% in February, excluding the Leap Year. February passenger throughput was 107% of 2019 levels, a decline from a year ago when throughput stood at 110% of 2019 levels owing to Leap Year. Although wage growth continues to outpace inflation, rising airfares could be a headwind to travel in 2025.

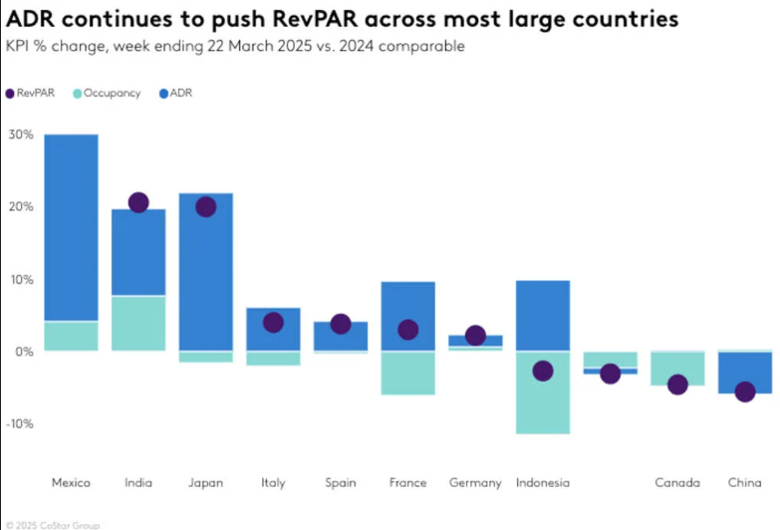

RevPAR Highlights

- Mexico continued to see strong performance as it has since last fall. Baja California, Mexican Caribbean, Cancun, and Mexico City led the strong growth with 12 of the 14 markets posting RevPAR growth driven primarily by ADR.

- India returned with strong RevPAR gains this week as 16 of its 17 markets reported increases. India also produced one of the top countries’ only occupancy gains (5.4ppts).

- Japan holds an equally strong position next to India, with ADR driving RevPAR growth. All 11 Japanese markets reported positive RevPAR

- Canada and the United Kingdom, two countries with travel patterns that often reflect those of the U.S., reported declining RevPAR due to decreases in occupancy.

Navigating uncertainty: Global air travel in a volatile economic and geopolitical landscape

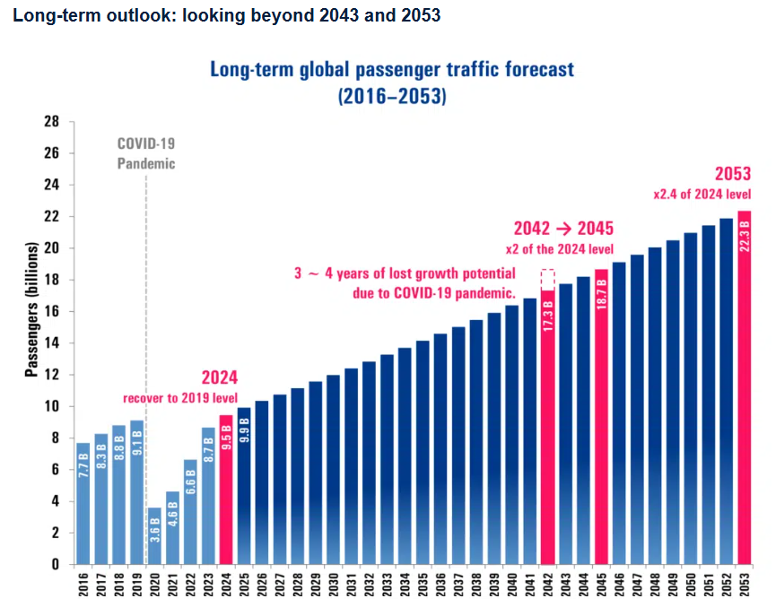

In 2025, global passenger traffic is forecast to reach 9.9 billion with a 4.8% YoY growth rate. While passenger demand remains strong, expansion is expected to slow as markets shift from recovery-driven surges to structural, long-term growth patterns.

Key challenges such as economic uncertainty, geopolitical tensions, and airline capacity constraints are expected to shape the industry’s trajectory increasingly. Demand stabilization, supply chain bottlenecks in aircraft production, and airport capacity shortages may temper growth in advanced markets. In contrast, high infrastructure investment and rising middle-class travel demand in emerging markets will likely continue to drive expansion. As the industry moves into a new era of growth, the airport industry must focus on financial viability, operational efficiency, and sustainability.

From 2024 to 2043, global passenger traffic is projected to grow at a compound annual growth rate (CAGR) of 3.4% to reach 17.7 billion passengers.

Based on the latest data, long-term forecasts now estimate a loss of 3 to 4 years of growth potential in global passenger traffic.

By 2045, passenger numbers will reach 18.7 billion, approximately doubling 2024. Looking further ahead, passenger traffic is forecast to reach 22.3 billion by 2053—approximately 2.4 times the 2024 projection—driven by a CAGR of 3% between 2024 and 2053.

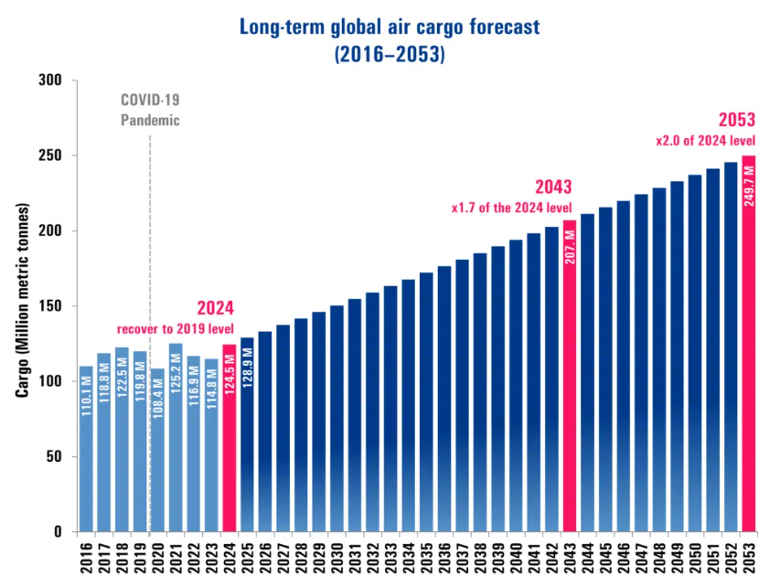

In 2024, the air cargo market is expected to reach 115 million metric tons (to be confirmed by ACI World in July 2025), reflecting nearly a 9% YoY growth rate and surpassing last year’s forecast.

In the long term, global air cargo volume is expected to grow steadily, with a projected CAGR of 2.7% between 2024 and 2043 and 2.4% between 2024 and 2053.

However, recent shifts in global trade policies, including the reintroduction of tariffs and rising trade tensions between major economies, introduce uncertainty into the long-term outlook. These evolving dynamics could impact supply chain efficiencies, trade flows, and air cargo demand.

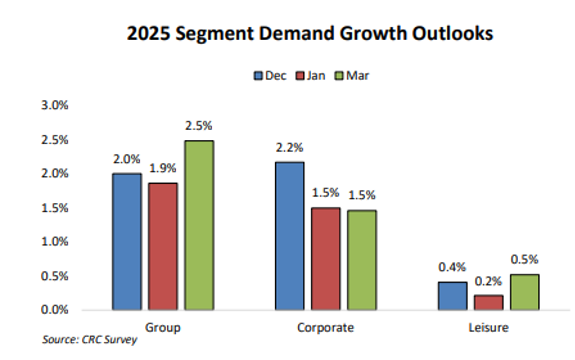

- Our March survey points to ’25 weighted average demand growth outlooks of 2.0% for Group, 1.5% for corporate, and 0.5% for leisure. This is 60bps better than our last group survey and unchanged for corporate and leisure.

- For the group,’25 pace continues to sound up 5-6% with room nights and ADR up 2-3% (slightly higher in ADR). We continue to see convention and corporate meetings driving the bulk of Group demand growth. For leisure, outlooks point to 0.5% growth, assuming a continuation of int’l inbound vs. outbound imbalance and most RevPAR growth coming from inflationary ADR increases. Based on our industry demand estimates, these outlooks suggest ~1.5% total US demand growth for ’25.

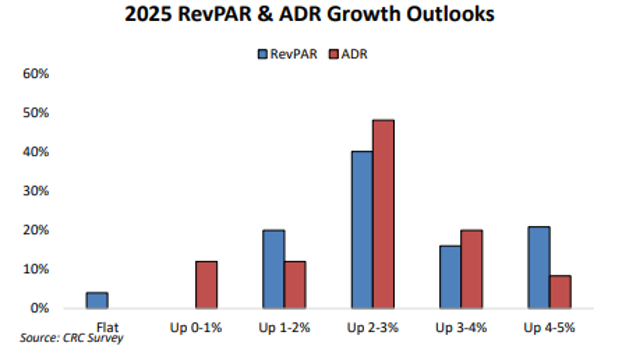

- ADR remains the key driver to ’25 RevPAR growth in current budgets. Our March survey points to a ’25 weighted average ADR growth of 2.1%, stable with our January survey.

- Based on our demand and ADR assumptions, we estimate 2.6% US RevPAR growth (prior 2.5%). Historically, late-cycle lodging demand has grown 1.5-2%. For ’25, we assume 1.3% demand growth, reflecting group and corporate up ~2% and leisure up ~0.5%. Assuming supply is up 0.8%, we expect slight occupancy growth (up 30bps). We assume 2.1% ADR growth, modestly underpricing inflation.

CBRE forecasts 2.4% 2025 GDP growth above the 2.1% long run. Inflation is expected to decrease in 2025, dropping to 2.5% from 2.9% in 2024

Alternative lodging sources continue to take shares from traditional hotels. The short-term rental demand share reached 13.5% in January 2025 compared with 11.3% at the beginning of 2020

CBRE forecasts RevPAR growth of 2.0% in 2025, accelerating to 2.6% in 2026. In 2025, CBRE expects a 1.6% increase in ADR and a 0.3% increase in occupancy to result in a 2.0% growth in RevPAR. Urban locations are expected to outperform other location types

Sources